Mat Accounting Entries Icai

Registrations For The Rajasthan Ptet 2019 Counseling Begins Counseling Online Registration Education

Guide To Minimum Alternate Tax For Ind As Compliant Companies

Osym Yks 2018 Basvurusu Nasil Ve Nereden Yapilir Egitim Final Sinavlari Universiteler

What Is The Concept Of Lease Equalisation Reserve And What Is The Accounting Treatment Quora

Icmai Cat January 2019 Exam Time Table And Programme Announced Bookkeeping Services Exam Time Accounting

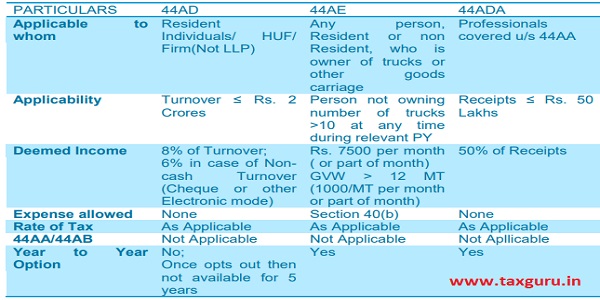

Practical Approach To Presumptive Taxation E Book

When the tax payable as per income tax provisions is higher.

Mat accounting entries icai. An issue has been raised whether the mat credit can be considered as a deferred tax asset within the meaning of accounting standard as 22 accounting for taxes on income issued by the institute of chartered accountants of india. In this case mat doesn t arise and hence accounting treatment is similar to the entry to be passed for provision for tax. The grant of credit for minimum alternative tax mat paid under section 115jaa of the income tax act 1961 has raised some issues regarding accounting for mat paid and the credit available thereon. Preparation of profit and loss account for the period before commencement of commercial operations.

However when the mat credit is not considered as a deferred tax asset it is still to be considered as an asset and the same should be classified under the head loans and advances. Icai is established under the chartered accountants act 1949 act no. Accounting for common fixed assets constructed for a project under progress. Mat credit may be considered as a deferred tax asset for the purpose of accounting standard as 22 which relates to accounting for taxes on income.

Icai the institute of chartered accountants of india set up by an act of parliament. Accounting treatment whether mat credit is a deferred tax asset 4. Information systems control and audit revised syllabus paper 7. Advanced management accounting.

Accounting for preliminary and other pre operative expenses. Direct tax laws relevant for may 2014 and november 2014 examinations paper 8. The differences between taxable income and accounting income for a period that originate in one period and are capable of reversal in one or more subsequent periods. Information systems control and audit.

Paper 5. Paper 6. This guidance note deals with the issues related to accounting and presentation of mat paid and carry forward of mat credit. Direct tax laws relevant for november 2013 examination paper 7.

Dear sir mat credit is utilised if income tax payable is more than mat so as per your question mat credit allowed in the earlier years but no entry is passed suppose for 2nd year provision for tax is 100 incometax mat is 80 mat credit entitlement a c has balance 20. Accounting for grants received. It is not appropriate to consider mat credit as a deferred tax asset for the purposes of accounting standard 22 accounting for taxes on income although mat credit is not a deferred tax asset under as 22 but it can be considered as an asset and the same should be presented under the head loans and advances considering it is of the nature.

Http Www Mastermindsindia Com Accounting 20for 20incomplete 20records Pdf

Company Accounts 1 Accounting For Share Capital Basic Concept In Hindi For 12th By Jolly Coaching Youtube

Ca Foundation Study Material Books Question Paper Download Free Sample Question Papers Test Papers More

How To Place Order Of Icai Books For New Student How To Get Ca Books In Icai Cds Portal In Hindi Youtube

Download Icai Ca Foundation Study Material Nov 2020 In English Hindi

Accounting Assumptions Going Concern Accrual And Consistency

How Do We Account For The Mat And Mat Credit Quora

Accounting Jugglery Abraham C Mathews Bw Businessworld

Account Assistant At Teleseen Marketing Pvt Ltd Careerfirst Accounting Jobs Assistant Jobs Bank Jobs

Download Icai Ca Cpt Study Material In Pdf Subject And Chapter Wise

Calculation Of Mat Credit Applicability Of Minimum Alternate Tax

Purchase Book And Purchase Return Book Introduction Solved Examples

Capital Funds And Special Funds In Non Profit Organisation Accounting