Mat Meaning In Income Tax

What Is Mat And How It Affects The Foreign Funds Taxact India Information Finance

Provision For Income Tax Definition Formula Calculation Examples

Rs 40 000 Standard Deduction From Fy 2018 19 Does It Really Benefit The Salaried Impact Of Standard Deduction On Yo Standard Deduction Deduction Income Tax

Misreporting Or Under Reporting Income Know Penalty Under Section 270a Of Income Tax Act Faceless Compliance

Individual Income Tax Faq Alabama Department Of Revenue

Federal Income Tax Tables 2019 Federal Tax Rate Deductions Credits Social Security Tax Rate Medicare Tax Federal Taxes Federal Income Tax

Income tax computed as per provision of section 115jb of income tax act.

Mat meaning in income tax. Under the provisions of section 115jb where the income tax calculated under the income tax act is less than 18 5 of the book profit then such book profit shall be deemed to the total income of the assessee and tax payable by the assessee shall be 18 5 on book profits. In this case mat is higher than the normal tax liability and hence the company is eligible for mat credit as per section 115jaa. Tax liability of a company for fy 2019 20 under normal provisions of the income tax act is rs. But here only mat on company s u s 115jb is discussed.

Mat a brief introduction. The mat credit is available in respect of mat paid under section 115jb of the income tax act 1961 with effect from asst. Due to increase in the number of zero tax paying companies mat was introduced by the finance act 1987 with effect from assessment year 1988 89. Meaning of book profit book profit is defined in the explanation 1 to section 115jb as book profit means the net profit as shown in the profit loss account for the relevant previous year and as increased and decreased by some prescribed items.

The promulgated ordinance reduced the mat rate of tax for ay 2020 21 to 15 per cent but did not amend section 115jaa related to mat credit. Minimum alternative tax is payable under the income tax act. In the case of a foreign company interest royalty or technical fees chargeable to tax under sections 115a to 115bbe or capital gain arising on transactions in securities if income tax payable in respect of these incomes under normal provisions other than provisions governing mat is less than the rate of mat applicable from the. In india mat is levied under section 115jb of the income tax act 1961.

With mat companies have to pay up a minimum amount of tax to the government. 10 000 or more during a financial year as computed in. The concept of mat was introduced to target those companies that make huge profits and pay the dividend to their shareholders but pay no minimal tax under the normal provisions of the income tax act by taking advantage of the various deductions and exemptions allowed under the act. 8 lakh while the liability as per the provisions of mat is rs.

The amount of mat credit would be equal to the excess of mat over normal income tax liability for which mat is paid during the said assessment year. Hence cbdt issued a circular no 29 2019 dated 02 10 2019 to clarify that a domestic company which availed the benefit of the reduced tax rate by using the option under section 115baa shall not be entitled to avail the brought forward mat credit. Under the income tax act 1961 every assessee has to pay tax in advance in case the advance tax liability is rs. It was introduced in the year 1987 and.

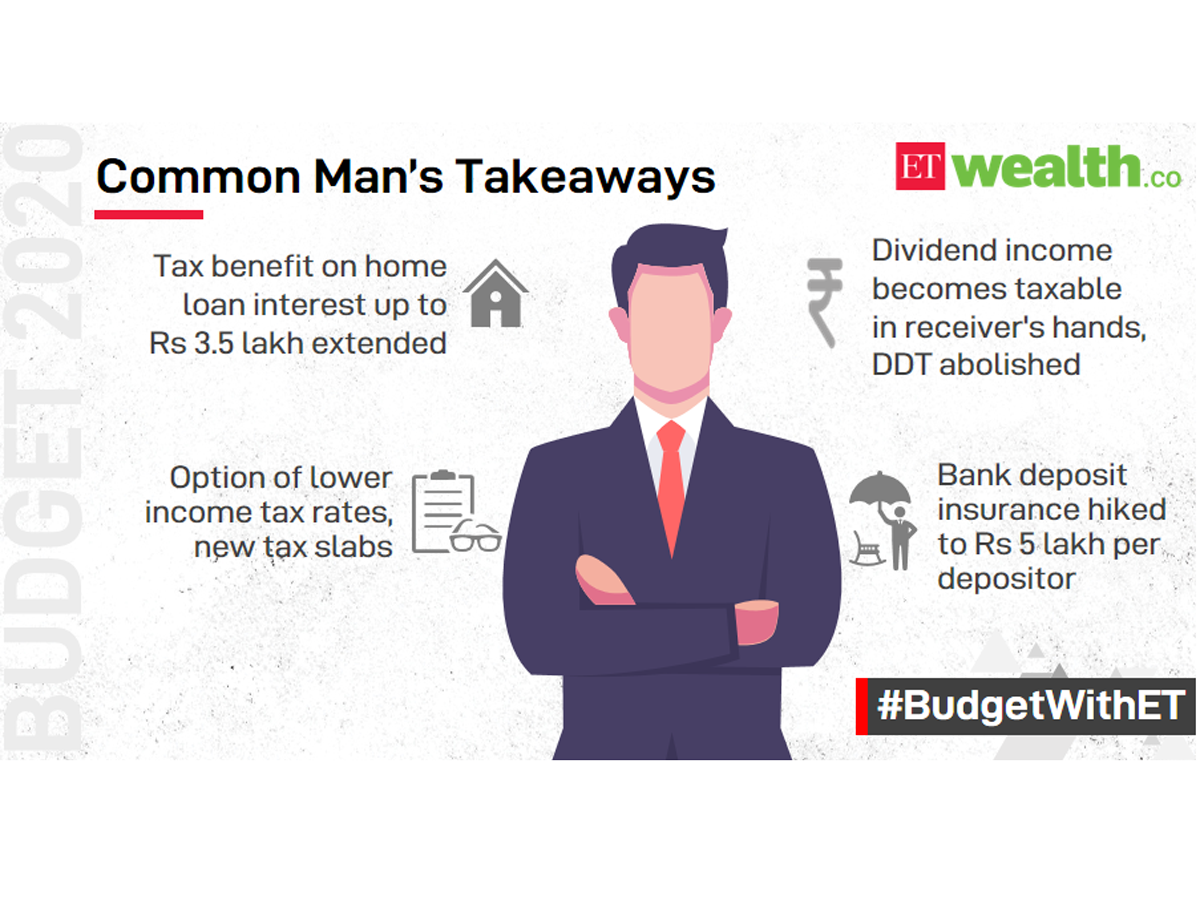

Income Tax Budget Announcements Income Tax Highlights Of Budget 2020 The Economic Times

Calculating Income Tax Payable Youtube

Rs 50000 Standard Deduction From Fy 2019 20 What Is The Impact On Your Taxable Income Standard Deduction Deduction Wealth Tax

Pin By Mat Uganda On Why Choose Mat Uganda Accounting Services Bookkeeping Services Accounting Firms

Benefitscommunication Communication Remind Workers Of These Tax Tips In 2020 Online Taxes Income Tax Return Tax Advisor

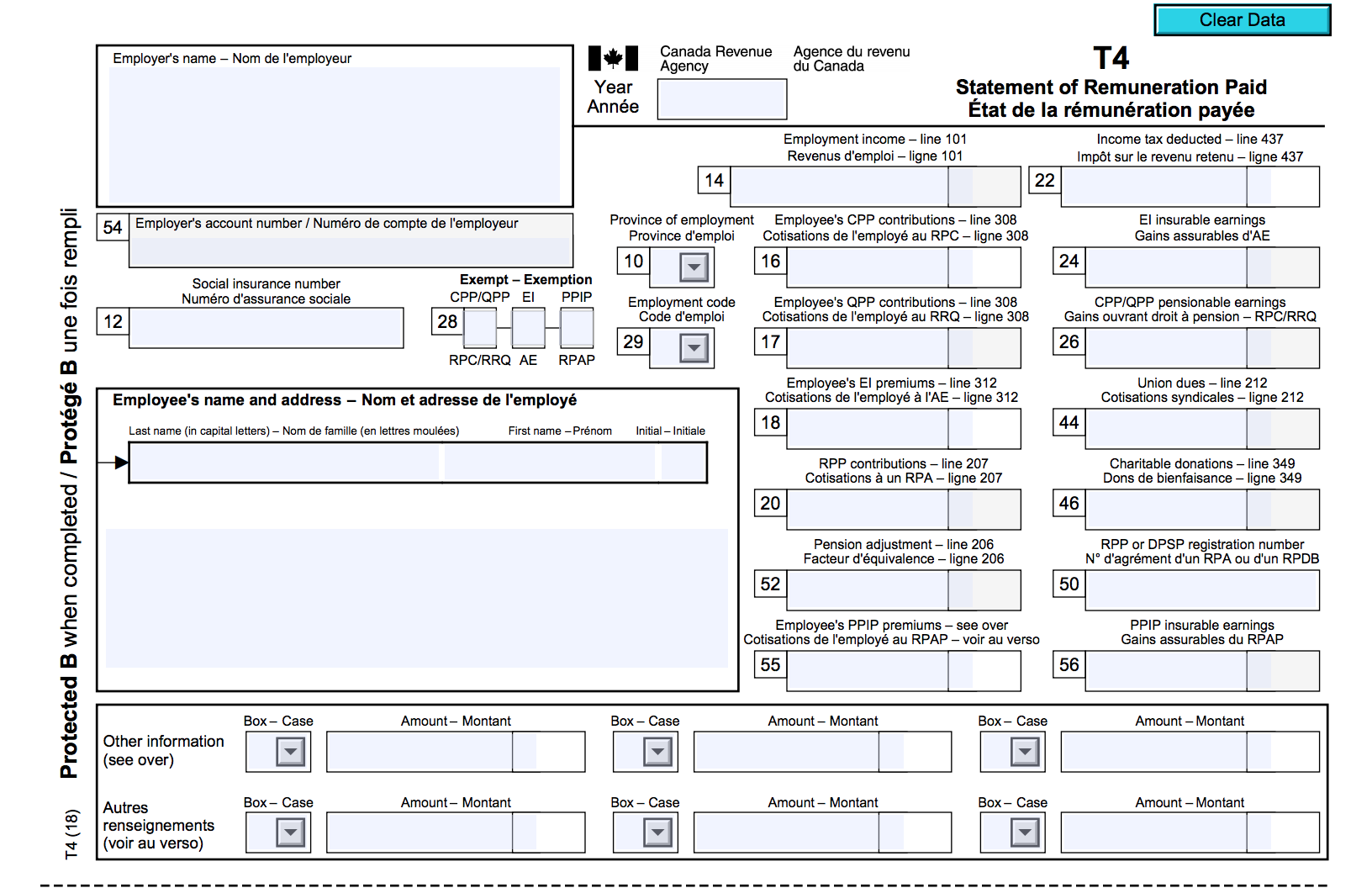

The Canadian Employer S Guide To The T4 Bench Accounting

Tax Returns Are Extremely Important For Every One Of Us One Really Needs To File His Returns On Time These Days O Tax Time Online Taxes Retirement Planning

Cbdt Allowed Employees To Claim It Exemption On Conveyance Allowance Under New Tax Regime In 2020 Tax Rules Paying Taxes Income Tax

When Is The Tax Extension Deadline For 2013 Tax Extension Tax Paying Taxes

This Is An Image 24811v08 Gif Tax Forms Irs Tax Forms This Or That Questions

While Calculating The Tax On Our Income We Are Well Aware Of The Income Tax Slab But We Need The Help Of Ca Or Any Ex In 2020 Tax Deductions Income

Pin By Lauren Kuperus On Diy Marketing Business Business Marketing

Foreign Tax Credit Form 1116 And How To File It Example For Us Expats