Mat Credit Utilisation Section

Analysis Of Taxation Laws Amendment Ordinance 2019 Zoho Blog

Caknowledge In Minimum Alternate Tax

Guide To Minimum Alternate Tax For Ind As Compliant Companies

Mat Credit Whether Credit For Surcharge And Education Cess On Brought Forward Mat Credit Is Available The Tax Talk

Https Www2 Deloitte Com Content Dam Deloitte In Documents Tax In Tax Minimum Alternate Companies Noexp Pdf

Minimum Alternate Tax Section 115jb How To Compute Arthikdisha

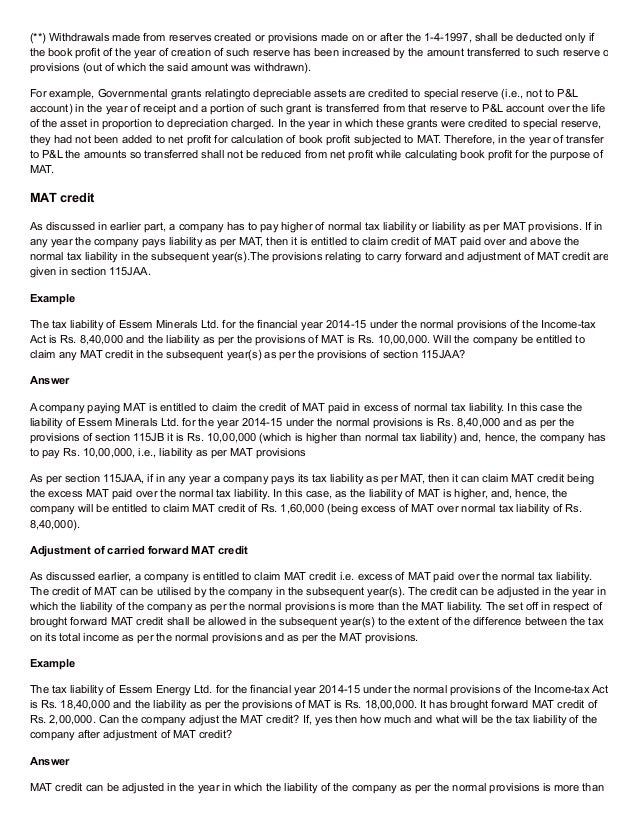

Mat credit under section 115jaa.

Mat credit utilisation section. Further whether mat credit is to be utilised in immediate previous year in which tax amt as per other provision exceeds the mat or it is optional for the assessee to choose the previous year in next 10 years for utilisation of credit. As stated above only the difference between mat paid and tax liability under provisions of the act is allowed to be carried forward as mat credit the cag has analysed 88 cases in 15 states wherein the assessee had received an undue benefit of under assessment by the assessing officer a o and consequently an undue carry forward of hefty mat. Mat credit shall be allowed to be set off in a year when the tax becomes payable on the total income in accordance with the normal provisions of the act. The mat credit is available in respect of mat paid under section 115jb of the income tax act 1961 with effect from asst.

As per section 115jaa if in any year a company pays its tax liability as per mat then it can claim mat credit being the excess mat paid over the normal tax liability. 5 2 as regards allowability or brought forward mat credit it may be noted that as the provisions of section 115jb relating to mat itself shall not be applicable to the domestic company which exercises option under section 115baa it is he clarified that the tax credit of mat paid by the domestic company exercising option under section 115baa of the act shall not be available consequent to exercising of such option.

Firms Opting For Lower Tax Regime Can T Adjust Accumulated Credits On Mat Business Standard News

Minimum Alternate Tax Mat Objective Applicability Calculation Of Mat Credit Finacbooks

Surcharge And Cess Is To Be Calculated After Deducting Mat Credit U S 115jaa From Tax On Assessed Income

The Bane Of Mat Credit

Consolidated Financial Statements Mindtree

Calculation Of Mat Credit Applicability Of Minimum Alternate Tax

Minimum Alternate Tax Mat Section 115jb

Re Measure Deferred Tax Assets Liabilities For Tax Rate Changes Ey India Business Standard News

Set Off Of Bf Loss Mat Credit Adjustments Under New Tax Regime

Https Assets Kpmg Content Dam Kpmg In Pdf 2020 01 Chapter 1 Aau Tax Ordinance Pdf

Improve Credit Score Improve Credit Score Improve Credit Credit Score Repair

Door Mat Credit Devhumor Door Mat Sweet Home Home

Tax Bill Typo In Tax Bill Bill Says Lower Mat Not This Year The Economic Times