Mat Credit Set Off Example

Up To 5 Mat Board Samples Can Now Be Ordered Online For Free Order Mat Board Samples When Color And Texture Is Critical Mat Board Sample Boards

Accounting Taxation Income Tax Slab Rates For A Y 2015 16 And 2016 17 Applicability Of Surcharge And Education Cess Income Tax Income Tax

Budget Calculator Spreadsheet Sample Template Free Budget Spreadsheet Template How To F Budget Spreadsheet Budget Spreadsheet Template Spreadsheet Template

Pin On Biology

The 12 Financial Rules You Need To Live By Sstofi Money Saving Plan Finances Money Budgeting Money

Advanced Financial Statement Analysis Templates In Word Doc And Excel Xls Financial Plan Template Financial Statement Analysis Business Plan Software

The question revolved on the question how advance tax has to be computed when the assessee has minimum alternate tax mat credit.

Mat credit set off example. The unavailed amount of mat credit entitlement if any should continue to be presented under the head loans advances. After claiming all applicable deductions exemptions and depreciation the gross taxable income comes out to be rs 4 lac. The amount of mat credit would be equal to the excess of mat over normal income tax liability for which mat is paid during the said assessment year. This mat credit can be carried forward and set off for 10 consecutive assessment years succeeding the year in which the tax credit first accrued.

500 200 300 100 200 3 1 000 200 1 200 1 200 200 total 800 500 1 300 4. The excess tax paid is allowed to be carried forward as mat credit. Mat credit can be better explained with the help of an illustration. Set off of mat credit brought forward is allowed to the extent of the difference between tax on total income and tax which would have been payable u s 115ja or u s 115jb as the case may be.

In the year of set off of credit the amount of credit availed should be shown as deduction from the provision of taxation on the liabilities side of the balance sheet. The set off rule and period may be different in different geographical locations. 1000 200 800 200 600 thus as per the above illustration in the year 4 opening debit balance to profit loss account is rs. The mat credit can be set off against tax payable in subsequent years up to ten assessment years immediately succeeding the assessment year in which the mat credit was earned.

Lower of loss or depreciation c f to next year. 1 300 100 400 400 100 2. In other words whether mat credit admissible in terms of section 115jaa of the income tax act has to be set off against the tax payable assessed tax before calculating interest under sections 234a b and c. So let s try to understand it with the help of an example.

115jaa 5 set off in respect of brought forward tax credit shall be allowed for any assessment year to the extent of the difference between the tax on his total income and the tax which would have been payable under the provisions of sub section 1 of section 115ja or section 115jb as the case may be for that assessment year. Book profit for mat. 115jaa does not expressly provide for set off of mat credit of the transferor company by the transferee company. Suppose a company abc books a profit of rs 8 lac.

Set off shall be allowed to the extent of difference between the tax on the total income under normal provision and tax which would have been payable as per mat under section 115jb.

Short Vowel Sound Word Lists Short A English Phonics Phonics Words Phonics

Gymnastic Equipment Gymnastics Equipment Gymnastics Room Gymnastics Equipment For Home

Vinyl Decals Order Form Sheet Letter Size Forms Sales Sheet Etsy Cricut Projects Vinyl Cricut Tutorials Cricut Projects Beginner

This Shopping List Template Includes Items That Are Sorted Into Categories Making It Easy To Shop For Shopping List Template Shopping List Apartment Checklist

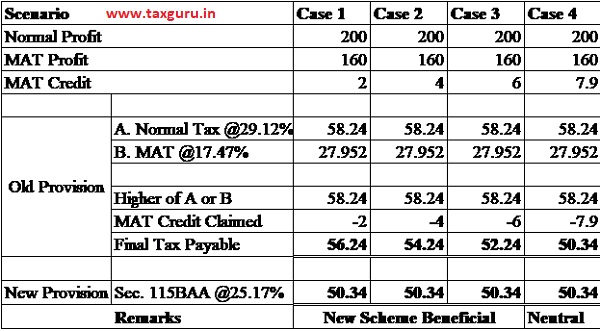

New Corporate Taxation Regime Section 115baa Mat

Unique Baby Checklist Pdf Exceltemplate Xls Xlstemplate Xlsformat Excelform Baby Checkli In 2020 Baby Shower Registry Baby Shower Checklist Registry Checklist

Reducing Fractions Battleship Reducing Fractions Fractions Fractions Resources

Here S A Story Plan That Includes A Picture Mat With Picture Tiles For Your Budding Writers They Can Use T Classroom Writing Writing Lessons Narrative Writing

Developing A Night Routine What Mine Looks Like Self Care Activities Night Routine Self Care

Geometry Raft Writing In Math Activity Math Writing Math Activities Maths Activities Middle School

Poster Grammar Punctuation 24x16in Grammar And Punctuation Learning Poster English Grammar

Basketball Practice Plan Template Excel Awesome Basketball Conditioning Workout Pdf Blog Dandk In 2020 Basketball Practice Plans Basketball Practice How To Plan

3 Letter Words With Z 3 Letter Word With Z In The Middle Gallery Letter Examples Ideas 3 Letter Word With 3 Three Letter Words 3 Letter Words Two Letter Words