Mat Credit Set Off Before Surcharge

Accounting Taxation Income Tax Slab Rates For A Y 2015 16 And 2016 17 Applicability Of Surcharge And Education Cess Income Tax Income Tax

Malaysia Airlines Enjoy Complimentary In Flight Meals Baggage Allowance And No Credit Card Surcharge When Tra Malaysia Airlines Discover Hong Kong Airlines

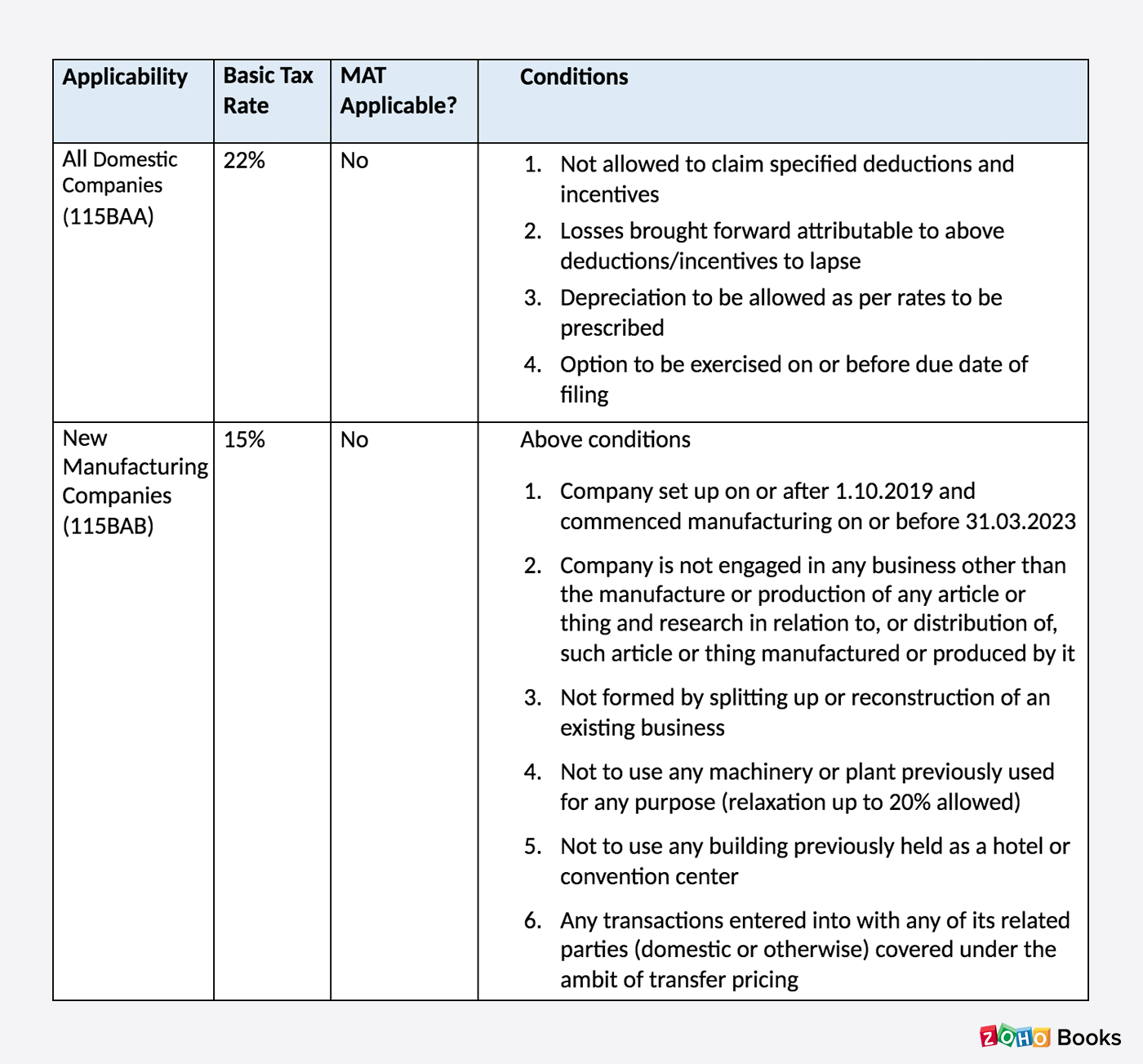

Analysis Of Taxation Laws Amendment Ordinance 2019 Zoho Blog

What Is The Applicable Minimum Alternate Tax Mat Rate For Ay 2020 21

Kyliecosmetics Red Shades Here Are Swatches Of The Kyliecosmetics Red Liquid Lipsticks Red Is My Favourite Go Red Liquid Lipstick Lips Shades Swatch

Pin On Home Decor Ideas

So far tax payer and tax authorities are concerned tax includes surcharge and cess in all aspects of tax administration.

Mat credit set off before surcharge. Set off shall be allowed to the extent of difference between the tax on the total income under normal provision and tax which would have been payable as per mat under section 115jb. The excess tax paid is allowed to be carried forward as mat credit. The mat credit can be set off against tax payable in subsequent years up to ten assessment years immediately succeeding the assessment year in which the mat credit was earned. As discussed earlier mat credit u s 115jaa is also about tax paid.

The set off rule and period may be different in different geographical locations. Taxpayer entitled for mat credit including surcharge cess. Mat credit to be allowed against tax including surcharge education cess. 115jaa has to be set off at a stage prior to levy of surcharge.

Particular head can be set off only against the income under the same head. On the same analogy brought forward tax credit u s. Ltd3 held that mat credit is to be calculated after taking surcharge and education cess into consideration. The tax paid is paid as per section 4 read with the finance act.

Mat credit shall be allowed to be set off in a year when the tax becomes payable on the total income in accordance with the normal provisions of the act. Accordingly the eligible mat credit available to set off for the company during the captioned a y needs to be arrived at by comparing the difference between the tax liability inclusive of surcharge and cess computed under the normal provisions of the act and the tax liability inclusive of surcharge and cess computed under the provisions. Pcit did not grant credit for surcharge and education cess on brought forwarded mat credit on the ground that term tax as defined under mat provisions in section 115jb for calculating book profit could not be extended to provisions for calculating carry forward and set off of mat credit. Application of the principal in relation to mat credit.

So only mat credit of tax paid is allowable. Ltd 4 held in favour of the tax department that for the purpose of carry forward and set off in subsequent years mat credit shall not include surcharge and cess. Surcharge at 5 shall be levied if book profit exceeds 1 crore. Before surcharge education cess with normal income tax payable.

Surcharge and education cess did not fall within. Allows carry forward set off of mat credit pursuant to hc sanctioned demerger. The dr supporting the order of the cit a submitted that there is a lot of difference between mat and tax rebate. Education cess 3 shall be added on the aggregate of income tax and surcharge.

It does not make any difference in tax calculation if the rates of surcharge and education cess remain same from year to year. He submitted that the assessee.

Pin On Plantillas

Dash Wellness Mat Flower Tile Nonslip Floor Mat World Market

Martha Stewart Collection 20 X 30 Spa Tub Mat Created For Macy S Reviews Bath Rugs Bath Mats Bed Bath Macy S

Deny Designs Heather Dutton Oh Christmas Tree Frost Bath Mat Reviews Bath Rugs Bath Mats Bed Bath Macy S

White Royal Blue Veritable Ankara Wax Print Fabric 100 Cotton Lustrous Quality Print Sold Per 6yds Price Is For 6yds Wax Print African Wax Print Printing On Fabric

Envelor All Purpose Interlocking Commercial Anti Fatigue Rubber Floor Mat 4 Pack 36 X 36 Reviews Bath Rugs Bath Mats Bed Bath Macy S

Gardenpath Plain Double Border Coir Door Mat Reviews Home Macy S

Wildkin Under Construction Nap Mat Reviews Bed In A Bag Bed Bath Macy S

Image May Contain One Or More People And People Standing Prom Dresses Long With Sleeves Top Prom Dresses Traditional Dresses

Waterhog Indoor Outdoor Mats Non Slip Door Mat

Hotel Collection Woven Stripe Cotton 18 X 26 Mat Created For Macy S Reviews Bath Rugs Bath Mats Bed Bath Macy S

How To Dress Up In Pastel Kawaii Fashion Outfits Really Cute Outfits Pastel Outfit

Kirmizi Kabartmali Hali Modeli Kirmizi Hali Dekorasyonlari Carpet Types Of Carpet Contemporary Rug