Mat Credit Meaning

Minimum Alternate Tax

Minimum Alternate Tax And Alternate Minimum Tax 115jb And 115jc

The Bane Of Mat Credit

Calculation Of Mat Credit Applicability Of Minimum Alternate Tax

Minimum Alternate Tax Mat Section 115jb

Https Www2 Deloitte Com Content Dam Deloitte In Documents Tax In Tax Minimum Alternate Companies Noexp Pdf

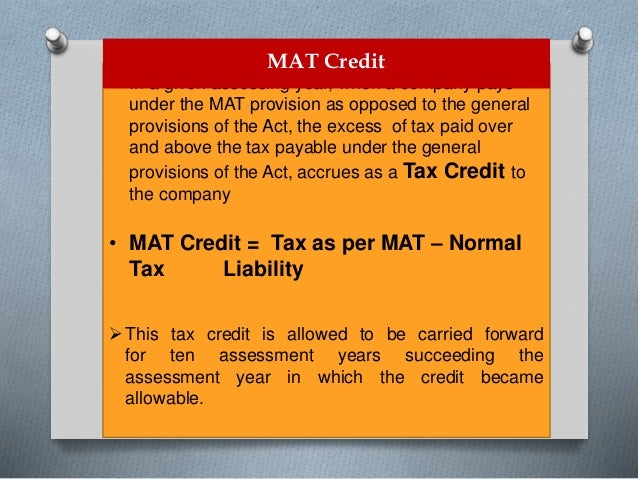

This mat credit is allowed a carry forward for a period of 15 financial years.

Mat credit meaning. Such tax credit shall be carried forward for 15 assessment years immediately succeeding the assessment year in which such credit has become allowable. Mat credit is the difference between the tax the company pays under mat and the regular tax. Mat or minimum alternate tax is a provision in direct tax laws to limit tax exemptions availed by companies so that they mandatorily pay a minimum amount of tax to the government. One can find provisions relating to carry forward and adjustment of mat credit in section 115jaa.

As per section 115jb all companies are required to pay corporate tax at least equal to the higher of the following. This is with effect from ay 2018 19 prior to which mat could be carried forward only for a period of 10 ays. Mat credit a new tax credit scheme is introduced by which mat paid can be carried forward for set off against regular tax payable during the subsequent seven year period subject to certain conditions as under. It was introduced to contain the practices followed by certain companies to avoid the payment of income tax even though they had the ability to pay.

Any company that pays minimum alternate tax under the mat clause instead of regular tax then if the tax paid is more than that accrued the excess amount is credited back as tax credit to the company. What is minimum alternate tax mat the concept of mat was introduced under ita to tax companies making high profits and declare dividends to their shareholders but have no significant taxable income because of exemptions deductions and incentives. If during a year a company has paid tax liability as per mat it is entitled to claim credit of excess of mat paid over the normal tax liability in the following year s. Mat is applied when the taxable income calculated as per the normal provisions in the it act is found to be less than 18 5 of the book profits.

Guide To Minimum Alternate Tax For Ind As Compliant Companies

Ways To Achieve And Repair Bad Credit Credit Card Tracker Credit Repair Credit Repair Business

Mat Vs Amt Minimum Alternate Tax And Alternative Minimum Tax Vakilsearch

What Is Minimum Alternate Tax Mat News Budget 2020 News Mat Calculation

Vocab Jam Learn 15 New Words With Everybody Wants To Be A Cat Nextstepenglish Com Good Vocabulary Words English Idioms Idioms And Phrases

Did You Know The Word Checkmate In Chess Comes From The Persian Phrase Shah Mat Meaning The King Is Helpless English Words Learn English English Idioms

Homograph Word Mat Homographs Same Word Different Meaning Words

Homonyms Word Mat Homonyms Words Homonyms Same Word Different Meaning

Pin On Istm

Checkmate Comes From The Persian Phrase Shah Mat Meaning The King Is Helpless Idioms And Phrases Linguistics Word Origins

Homonyms Word Mat English Ks2 Ks3 Homophones Words Homonyms Words Grammar For Kids

Capital Market Instruments Traded Meaning Functions Credit Card Help Capital Market Marketing

Mat Vs Amt Minimum Alternate Tax Alternate Minimum Tax Indiafilings