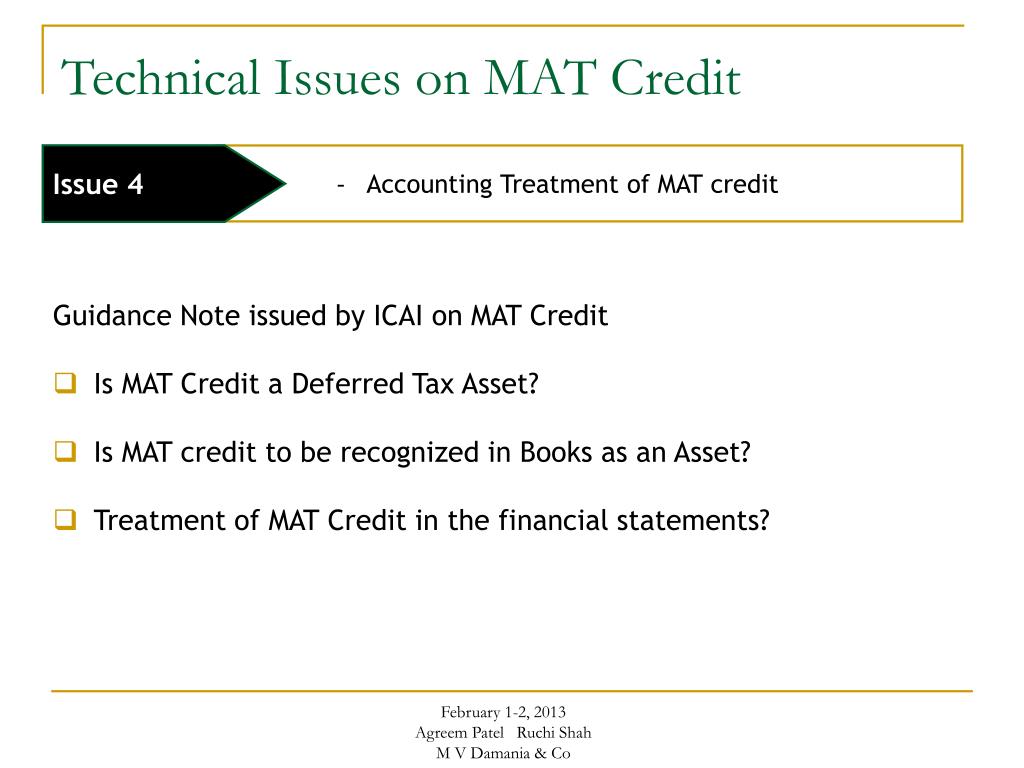

Mat Credit Accounting Treatment

Accounting Taxation Income Tax Slab Rates For A Y 2015 16 And 2016 17 Applicability Of Surcharge And Education Cess Income Tax Income Tax

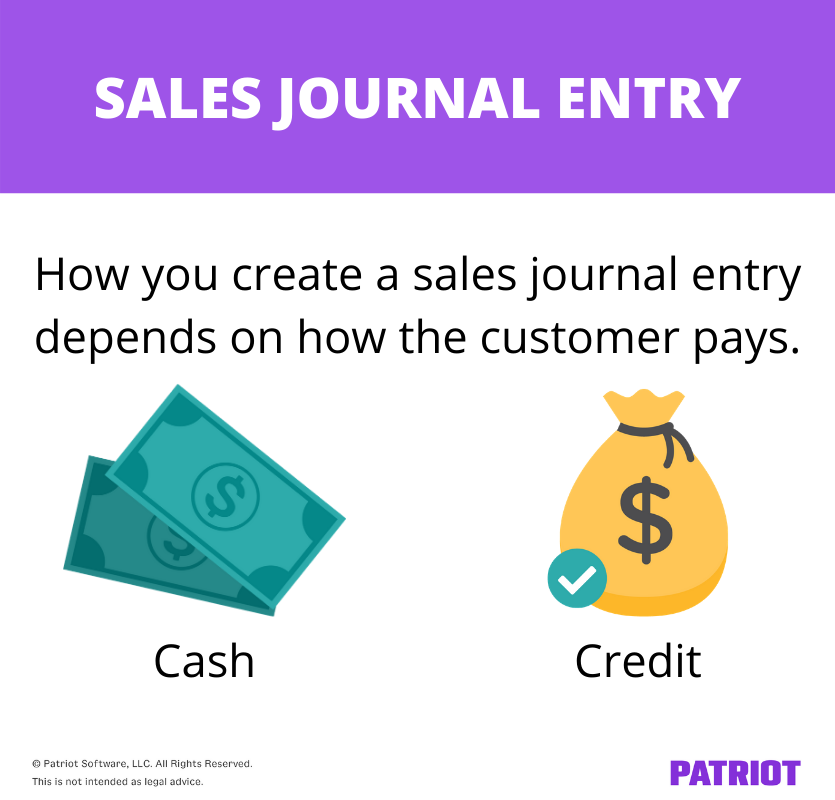

Sales Journal Entry Cash And Credit Entries For Both Goods And Services

Guide To Minimum Alternate Tax For Ind As Compliant Companies

Acx Program Is Awesome Spend 10 Make Back 15 In Just 40 Days Spend 100 000 Make Back 150 000 Http Www Adclickxpr Send Money Accounting Online Income

Accounting Swear Words Finance Office Humor Poster Zazzle Com Accounting Humor Words Finance

Bluedarkaccountingbackground Illustration Calculations Mat In 2020 Gold Calculator Mockup Identity Mathematics Education

According to as 22 deferred tax asset arise on account of differences in the items of income and.

Mat credit accounting treatment. Mat credit is not a deferred tax asset as per as 22 on accounting for taxes on income issued by icai deferred tax liability or deferred tax asset arises on account of timing differences i e. It has been proved that payment of mat does not result in any timing difference since it does not give rise to any difference between the accounting income and taxable income. The differences between taxable income and accounting income for a period that originate in one period and are capable of reversal in one or more subsequent periods. Mat under p l a c dr 100 mat credit under lo.

The differences between taxable income and accounting income for a period that originate in one period and are capable of reversal in one or more. Accounting treatment whether mat credit is a deferred tax asset 4. Lets assume that income tax is 100 mat is 120 you ll have to pay 120 and a credit of the difference between both the amounts will be granted to you. Mat credit may be considered as a deferred tax asset for the purpose of accounting standard as 22 which relates to accounting for taxes on income.

Mat credit is not a deferred tax asset as per as 22 on accounting for taxes on income issued by icai deferred tax liability or deferred tax asset arises on account of timing differences i e.

Strongesttyphoons Science Climate Change Sayings

Ppt Minimum Alternate Tax Section 115jb Powerpoint Presentation Free Download Id 4406076

Carson Daly Father Under Carsen Edwards Of The Purdue Boilermakers Plus Cars 3 Toys Wherever Cars 3 Florida Speedway Under Car Life Help Useful Life Hacks Tips

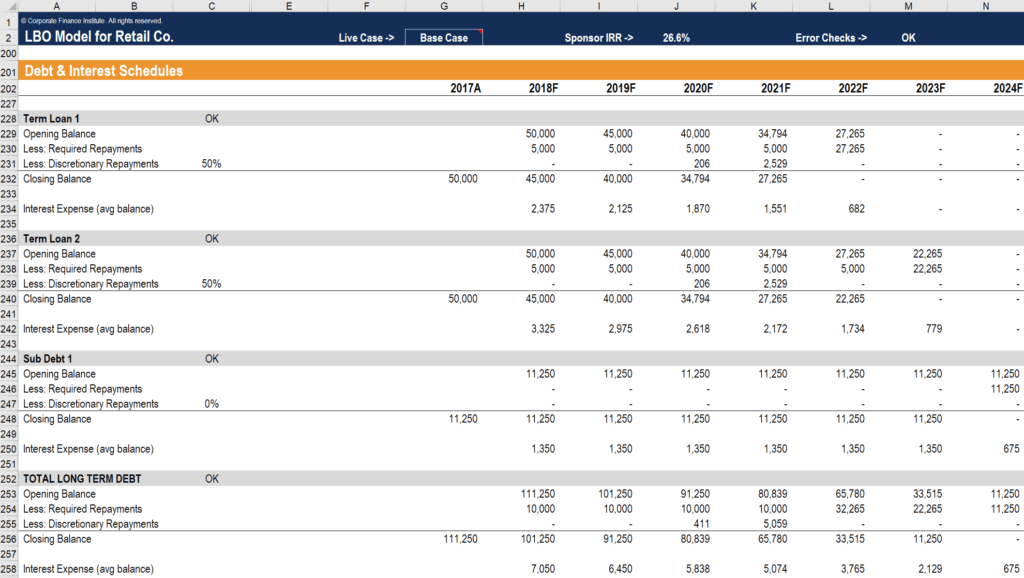

Debt Schedule Timing Of Repayment Interest And Debt Balances

New Details On The Canada Emergency Wage Subsidy

Get Debt Relief For Credit Cards Medical Bills Other Unsecured Debt And Tax Debt Today Taxes Humor Accounting Humor Accounting Jokes

Church Management System Church Database Software Churchapp Album Songs Book App Work From Home Opportunities

How To Protect Bank Accounts From Hackers Easy Ways To Protect Your Bank Account Itechnhealth Com Bank Account Online Bank Account Banking App

Core I5 3rd Gen Toshiba Affordable In 2020 Toshiba Laptop Pouch Ms Office

Receipt Accounting Chapter 2 20c

Financial Accounting Flashcards Quizlet

Deferred Tax Liability Accounting Double Entry Bookkeeping

693 24 Wallpaper Of Wedding Ideas Di 2020