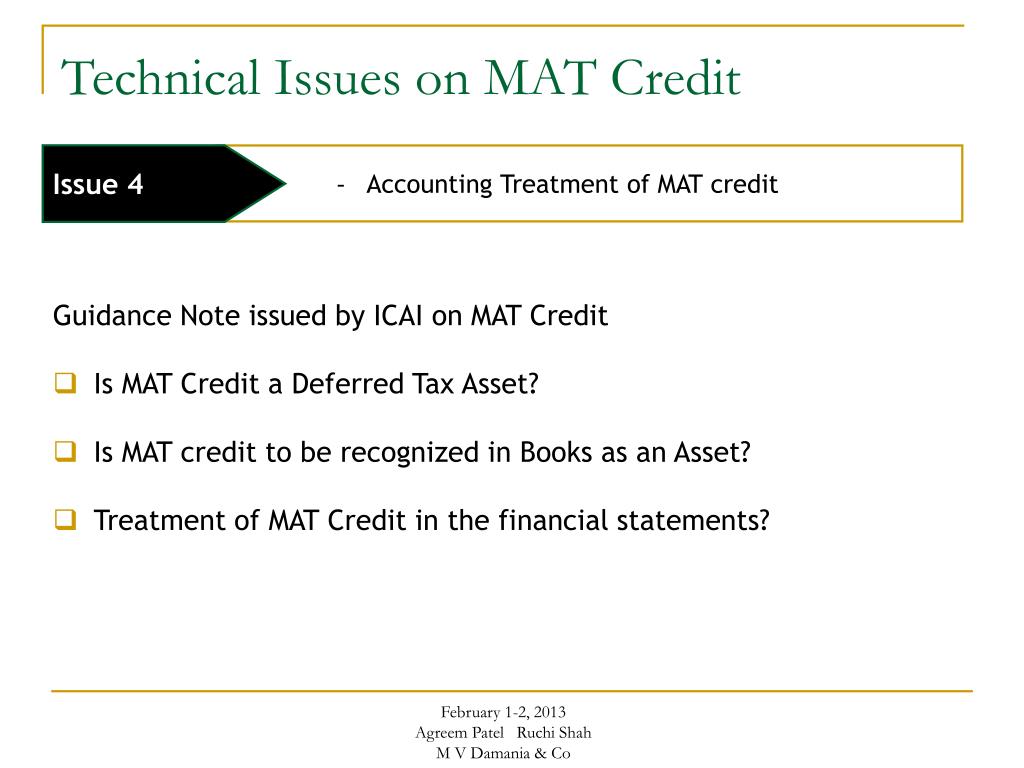

Mat Credit Accounting Guidance Note

Quick Studyguide Accounting Notes Handwriting Exams Studytips Collegelife Reviewguide Accounting Notes School Study Tips Study Notes

Guide To Minimum Alternate Tax For Ind As Compliant Companies

Learn Accounting Online Learn Accounting Financial Management Accounting

Pin On Blank Check

25 It Help Desk Resume Examples Cover Letter Templates

23 Internal Job Posting Template Event Planning Quotes Cover Letter Template Business Plan Template

1 whether mat credit is a deferred tax asset.

Mat credit accounting guidance note. 1983 times file size. Mat credit may be considered as a deferred tax asset for the purpose of accounting standard as 22 which relates to accounting for taxes on income. The guidance note on accounting for credit available in respect of minimum alternative tax under the income tax act 1961 as issued by icai gn a 22 issued 2006 further stipulated that. Guidance note on accounting for credit available in respect of minimum alternative tax under the income tax act 1961 guidance note on accounting for real estate transactions revised 2012 guidance note on measurement of income tax for interim financial reporting in the context of as 25.

It may be noted that the institute had in the year 1997 issued a guidance note on accounting in respect of minimum alternative tax which dealt with the recognition. On 18 may 2009. This guidance note to deal with the aspects of accounting and presentation of mat paid and the credit available in this regard. The guidance note on accounting for mat credit suggests the following.

Full guidance note including treatment in accounts in response to provisions of i t. Mat credit is an asset because it can be used in the future within specified period to set off mat credit against the normal tax liability and hence it. However when the mat credit is not considered as a deferred tax asset it is still to be considered as an asset and the same should be classified under the head loans and advances. Mat credit is not a deferred tax asset as per as 22 on accounting for taxes on income issued by icai deferred tax liability or deferred tax asset arises on account of timing differences i e.

Guidance note on accounting for credit available in respect of minimum alternative tax under the income tax act 1961 23 03 06. Other files by the user. In which mat credit becomes eligible to be recognized as an asset in accordance with recommendations contained in this guidance note the said asset should be created by way of a credit to the profit loss account presented as a separate line item therein. Act 1961 pdf submitted by.

The grant of credit for minimum alternative tax mat paid under section 115jaa of the income tax act 1961 has raised some issues regarding accounting for mat paid and the credit available thereon. Mat credit entitlement will be treated as an asset and the accounting will be done by crediting the profit loss a c if there is a virtual certainty that the company will be able to recover the mat credit entitlement in future limited period.

Receipt In Store Document Store Money Template Passport Template Receipt Template

Ppt Minimum Alternate Tax Section 115jb Powerpoint Presentation Free Download Id 4406076

Complete Controller Offer You A Complete Bookkeeping Services In Seattle Wa To Small And Large Businessman Jus With Images Accounting Jobs Bookkeeping Services Bookkeeping

Scary Accounting Accountant Halloween Funny Mouse Pad Zazzle Com Accounting Jokes Accounting Humor Accounting

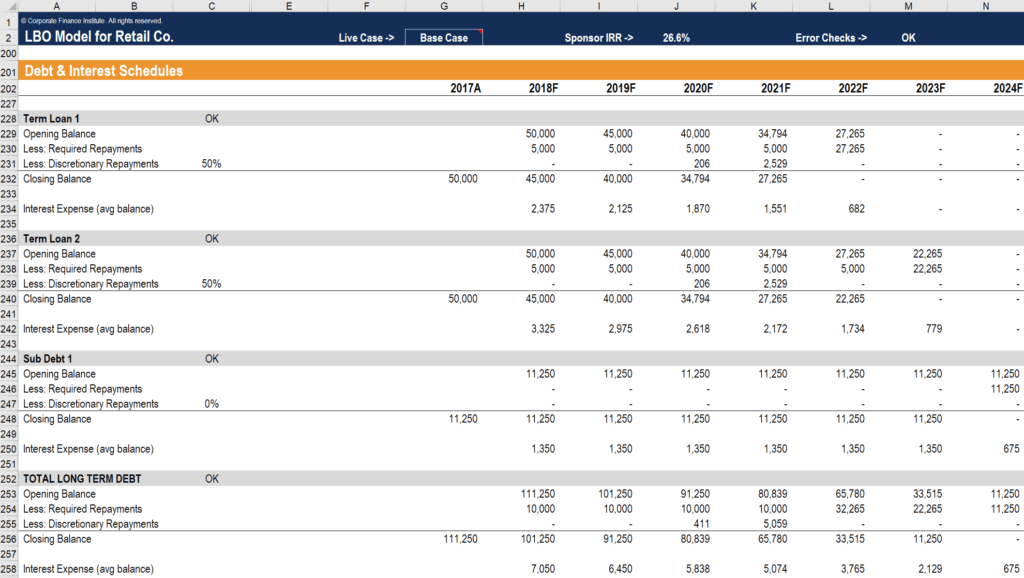

Debt Schedule Timing Of Repayment Interest And Debt Balances

Instant Pay Stub Maker Check Stub Maker Business Checks Congratulations On Your Achievement Statement Template

New Details On The Canada Emergency Wage Subsidy

Pdf Luca Pacioli S Double Entry System Of Accounting A Critique

Https Www2 Deloitte Com Content Dam Deloitte In Documents Tax In Tax Minimum Alternate Companies Noexp Pdf

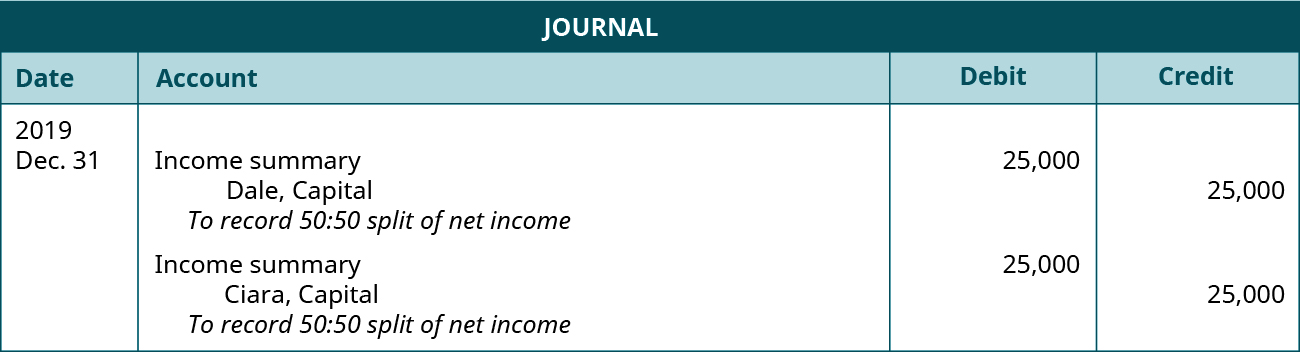

Compute And Allocate Partners Share Of Income And Loss Principles Of Accounting Volume 1 Financial Accounting

Pin By Teresa Mcmillan On Accounting Is Fun Well It S Useful Accounting Jokes Accounting Humor Accounting Office

Demystifying Number System Practical Concepts And Their Applications For The Cat And Other Mba Exams Online College Online Psychology Degree Finance Career

Provision For Taxation Accounting Treatment All About By Ca Parveen Sharma Youtube