Mat Calculation In Income Tax

How To Calculate Net Income 12 Steps With Pictures Net Income Formula In 2020 Net Income Income Net

Income Tax Slab Rates For Fy 2019 20 Ay 2020 21 Budget 2019 20 Key Highlights Tax Forms Income Tax Wealth Tax

Rs 40 000 Standard Deduction From Fy 2018 19 Does It Really Benefit The Salaried Impact Of Standard Deduction On Yo Standard Deduction Deduction Income Tax

Learn How To Report And Pay Taxes On Your 1099 Income Paying Taxes Income Tax Return Income

Income Tax Exemption Vs Tax Deduction Vs Tax Rebate Vs Tds Key Differences Tax Deductions Income Tax Tax Exemption

Calculating Income Tax Payable Youtube

The amount of tax and surcharge cannot exceed the tax calculate under marginal relief.

Mat calculation in income tax. However the rate of income tax under section 115jb shall be reduced rate of 15 percent instead of 18 5 per cent with effect from assessment year commencing on or after the 1st day of april 2020. Step 2 adjustment to net profit to convert it into book profit which are given under explanation 1 to section 115jb. As per section 115jb every taxpayer being a company is liable to pay mat if the income tax including surcharge and cess payable on the total income computed as per the provisions of the income tax act in respect of any year is less than 18 50 of its book profit surcharge sc health education cess. It is calculated under section 115jb of the income tax act.

Tax liability as per the normal provisions of income tax act tax rate 30 plus 4 edu cess plus surcharge if applicable. Payable tax cannot be less than the 18 5 of book profit in an assessment year the mat rate has been reduced to 15 from fy 19 20. Since income exceeds 1 crore marginal relief is to be calculated i e. Assessing officer s power to alter net profit.

Mat is calculated under section 115jb of the income tax act. There are specific provisions under the income tax act 1961 under which the mat is collected from every company. Now compute tax payable as per mat provisions tax payable 18 5 surcharge 7 19 795 of 1 01 00 000 19 99 295. It means the rate of mat is reduced to 15 percent from the ay 2020 21 itself.

Rs 50000 Standard Deduction From Fy 2019 20 What Is The Impact On Your Taxable Income Standard Deduction Deduction Wealth Tax

Hurdle Rate Definition And Example Guide To Hurdle Rates Within Tax Rate Formula In 2020 Excel For Beginners Tax Rate Finance Jobs

Federal Income Tax Tables 2019 Federal Tax Rate Deductions Credits Social Security Tax Rate Medicare Tax Federal Taxes Federal Income Tax

Individual Income Tax Faq Alabama Department Of Revenue

Best Tax Return App To File Income Tax Return For Fy 2018 19 You Can Upload Your Form 16 Itr In This App An Income Tax Return Tax Return Income Tax

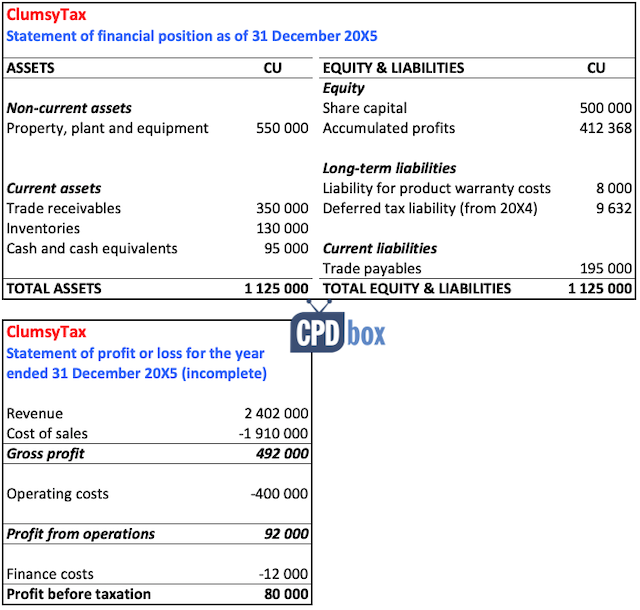

Tax Reconciliation Under Ias 12 Example Ifrsbox Making Ifrs Easy

Georges Excel Mortgage Calculator Pro V4 0 Mortgage Calculator Mortgage Payment Calculator Mortgage Amortization

How Much You Owe The Irs Self Employment Tax Calculator Federal Income Tax Tax Self Employment

Daily Updates 11th March 2020 In 2020 Yes Bank

In203 Medical Insurance Basics Medical Insurance Health Insurance Cost Medical

Image From Http Www Fdlcu Com Uploads Basic 20budget 20worksheet1 Jpg Budgeting Worksheets Budgeting Personal Budget

Foreign Tax Credit Form 1116 And How To File It Example For Us Expats

Daily Updates 11th March 2020 In 2020 Yes Bank