Mat Calculation As Per Ind As

Guide To Minimum Alternate Tax For Ind As Compliant Companies

Cbdt Circular Of Clarifications Faqs On Computation Of S 115jb Book Profit For Ind As Useful Miscellania

What Is The Applicable Minimum Alternate Tax Mat Rate For Ay 2020 21

Guide To Mat With Ind As Impact On Mat Computation 2019

How To Calculate Profit Or Loss From Balance Sheet Http Www Svtuition Org 2014 11 How To Calculate Profi Accounting Education Learn Accounting Balance Sheet

Tens Frame Work Mat For Addition And Subtraction Elementary Math Ten Frame Math Addition

Under existing rules book profit is calculated as per section 115jb of the income tax act 1961.

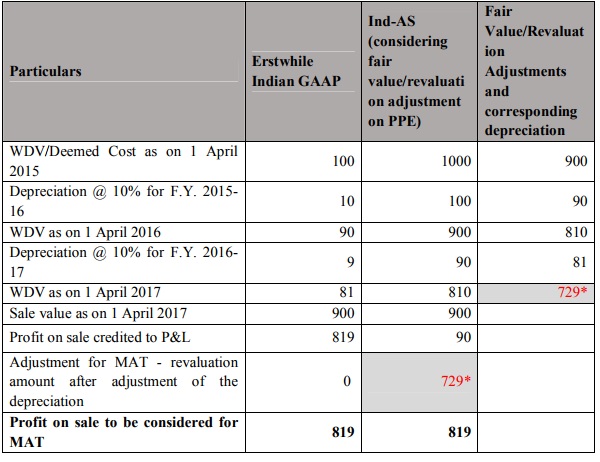

Mat calculation as per ind as. Hence the transition amount will be adjusted 1 5 th each year in 2017 18 to 2021 22. Then the transition amount will be adjusted under mat equally in five consecutive years starting from 2017 18. Calculation of book profits for the purpose of mat maximum alternate tax section 115jb for computation of book profit one may proceed as follows. Any loss arising out of fair value adjustments of financial instruments measured at fair value.

Mat is applicable to all companies including foreign companies. The starting point for mat computation is profit before other comprehensive income oci and not the total comprehensive income. Para 11 of appendix a to ind as 10 provides that any distributions of non cash assets to shareholders for example in case of a demerger shall be. Since income exceeds 1 crore marginal relief is to be calculated i e.

As per ind as 101 a company would make all ind as adjustments on the opening date of the comparative financial year. Clause c and d of section 115 2a and section 115 2b have to be read in conjunction to understand the calculation of mat in a scheme of demerger of companies that are following ind as. Every company should pay higherof the tax calculated under the following two provisions. Mat on ind as compliant financial statement i for mat calculation the starting point is the net profit as per the statement of profit and loss before considering any items forming a part of other comprehensive income oci.

Xyz limited is adopting indian accounting standards ind as for the first time in financial year 2017 18. As per the concept of mat the tax liability of a company will be higher of the following. Tax liability of the company computed as per the normal provisions of the income tax law i e tax computed on the taxable income of the company by applying the tax rate applicable to the company. Minimum alternate tax calculation example.

The taxable income of abc company not availing any tax exemptions incentives as per the provisions of the income tax act 1961 is rs. Summary of clarifications issued by the cbdt on the mat provisions applicable to ind as reporters. The entity is also required to present an equity reconciliation between previous indian gaap and ind as amounts both on the opening date of preceding year as well as on the closing date of the preceding year. The amount of tax and surcharge cannot exceed the tax calculate under marginal relief.

This article discusses the amendments made to section 115jb to incorporate adjustments as mandated by ind as. Mat is calculated as 15 of the book profit of the tax assesse. Mat is calculated under section 115jb of the income tax act.

Calculation Of Mat Credit Applicability Of Minimum Alternate Tax

Pin On 3d Modeling Design

6174 Is Known As Kaprekar S Constant After The Indian Mathematician D R Kaprekar Tripleleap Sunday Didyouknow Mat Mathematician Mathematics Subtraction

Zeal Silicone Baking Mat With Measurements Baking Baking Cookie Sheets Bakeware Set Silicone Baking Mat

Hematite For Door Protection In 2020 Reiki Healing Crystals Hematite Crystal Reiki Crystals

Rug Rag Braided Round Rug Meditation Mat Mandala Rug Bohemian Decor Colourful Area Rug Home Decor Rug Floor Rug Floor Rugs Braided Rag Rugs Rugs On Carpet

Pin By Mesele Kinfe On Excel Spreadsheets In 2020 Bridge Design Civil Engineering Design

1 Hand Braided Bohemian Cotton Chindi Area Rug Ivory Colors Home Decor Rugs Cotton Area Rug Size 3x5 Rectangle Size Braided Rag Rugs Oval Rugs Rag Rug

Vastu Shastra In Tamil Tamil Vastu Feng Shui Astrology In Tamil Tarot Reading In Tamil Vastu In Tamil Vastu Shastra Feng Shui Astrology Kitchen Vastu

Satta Matka Guessing 143 Bossmatka Top Kalyan Mumbai Matka 03 August Kalyan Chart Satta Matka King

Vinyl Cost Calculator Craft Pricing Calculator Cost Sheet Printable Vinyl

Pin On Tg Struc

Indian Calculation Gernal Knowledge General Knowledge Facts Knowledge Quotes